A response we hear repeatedly in conversations with developers about BESS project valuation.

What is often underestimated is that financing assumptions, depending on revenue structure and project size, have a significant impact on potential project value and should therefore be considered.

In valuations, assumptions from the PV world are often applied first: 70–80% debt with an annuity loan.

👉 This logic cannot be automatically transferred to BESS.

Merchant revenues and their intra-year volatility often lead to different bankable structures.

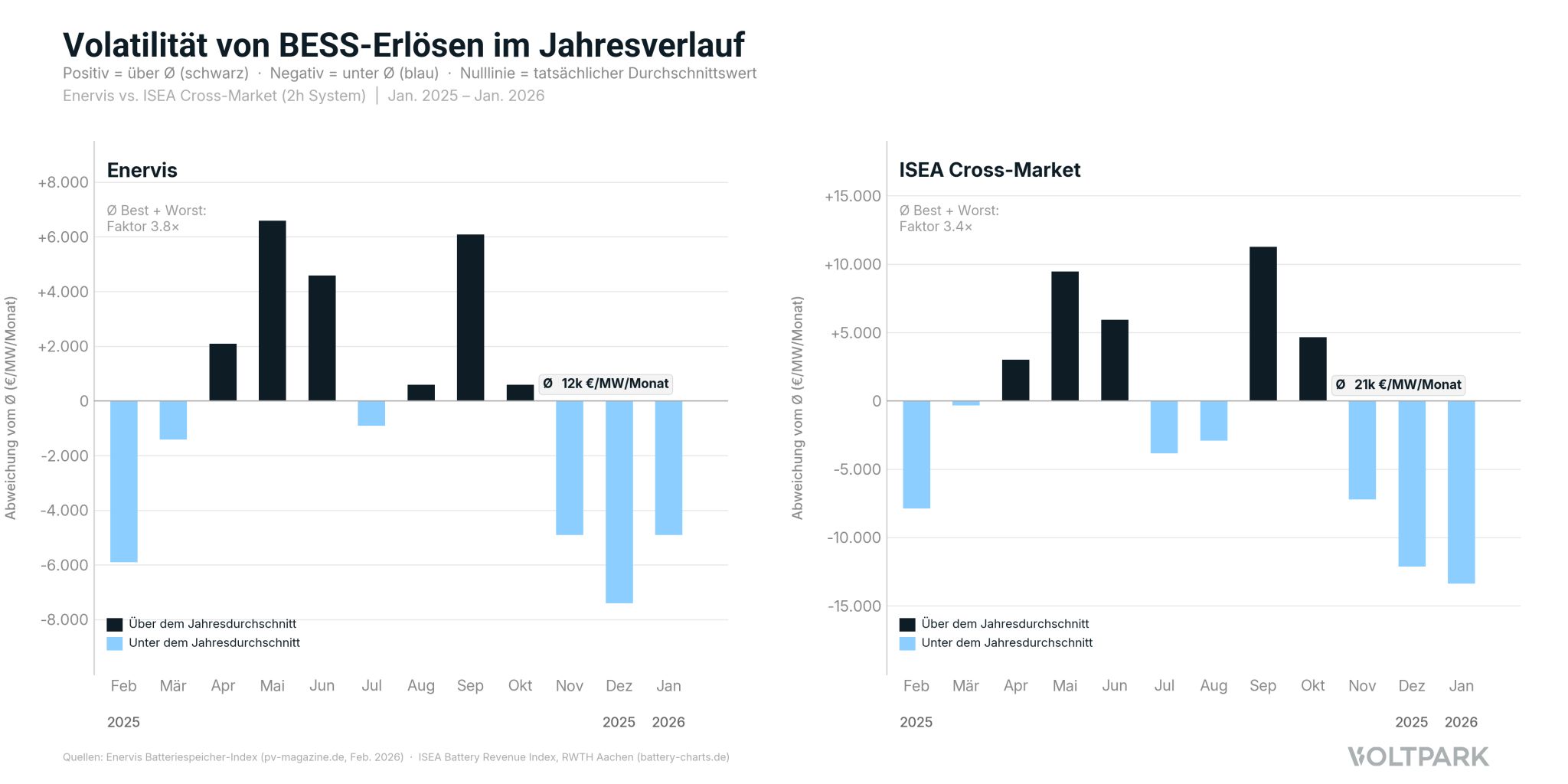

Factor 3.8x and 3.4x: The Monthly Spread in BESS Revenues (DE)

According to the Enervis Battery Storage Index and ISAE Battery Charts Revenue Index (1 MW / 2 MWh, 2025):

1. Merchant Revenues with Potential FCA Restrictions Mean Significantly Higher DSCR Requirements

Without contractually secured cash flows, structuring becomes more conservative. Result:

➡️ Lower bankable debt base

✅ Higher equity requirements

2. Banks Address Volatility Through Sculpted Debt

Repayment follows expected cash flow: higher payments in strong periods, lower in weak ones. However, such financing must be properly structured and contractually secured.

3. For Smaller Projects (<10 MW), Structuring Can Become Uneconomical

When debt sizing is very conservative, the debt volume can be so small that structuring and transaction costs for the bank (DD, banking process, etc.) are disproportionately high. In such cases, financing must be entirely through equity, which in turn increases the return requirements for the project.

4. Bank-Friendly Alternative: Floor or Tolling Models

They secure minimum cash flows, reduce DSCR requirements, and improve bankability.

Trade-off: Additional structuring effort and part of the upside is given up.

Conclusion

For BESS, financing is not a downstream investor concern, but an aspect that developers must also consider.

Anyone evaluating or developing projects should be clear about realistic and evolving financing assumptions (DSCR requirements, tolling/floor, sizing logic).