Negative power prices were long considered a summer phenomenon: PV peaks at midday meeting low demand. This logic is shifting. With growing PV and wind capacity, even spring days now suffice to produce surpluses.

Q1 Year-on-Year: The Trend Is Clear

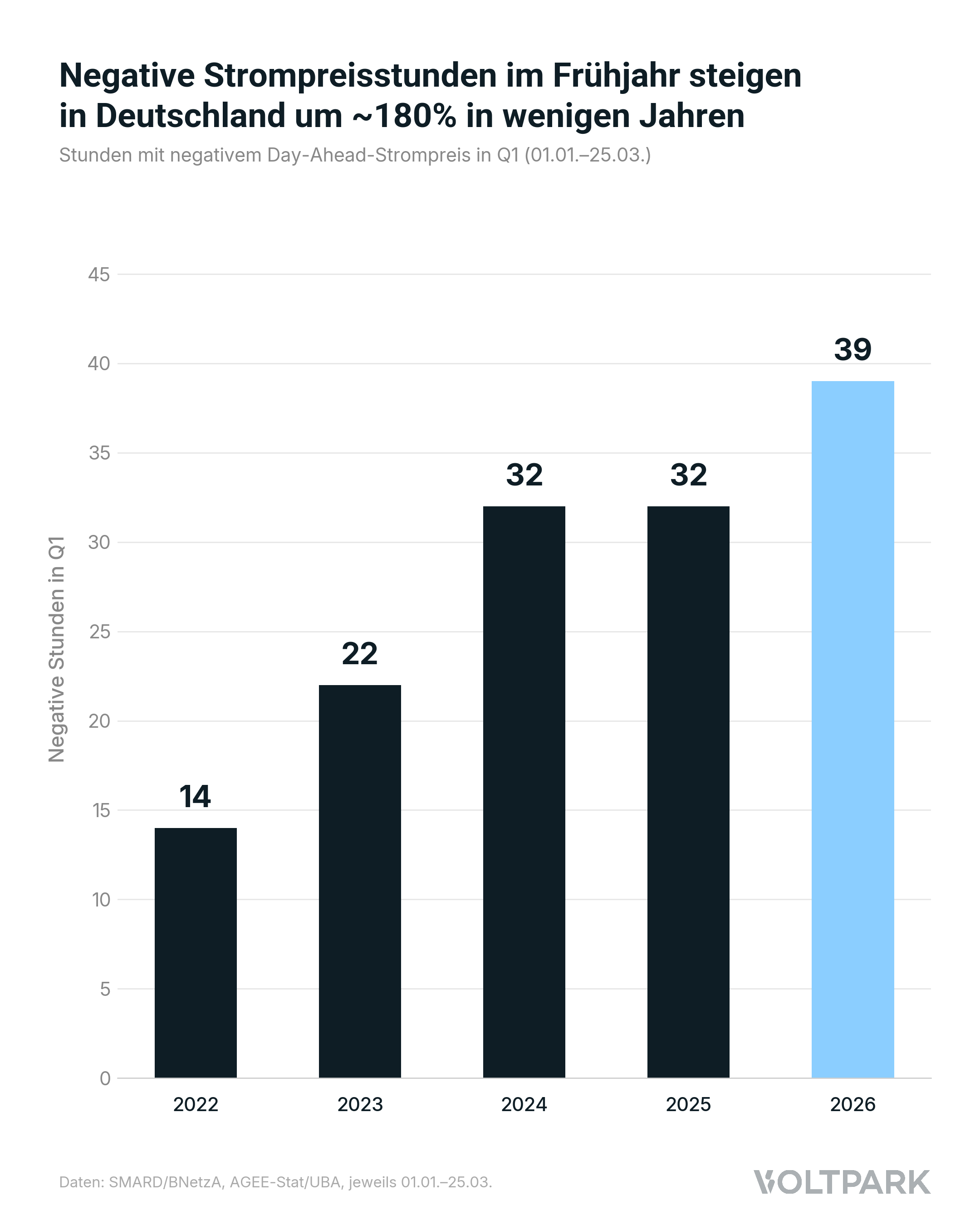

Cumulative for the period Jan 1–Mar 25 (EPEX Spot DE/LU): Q1 2022 had 14 negative hours. Q1 2023 reached 22. 2024 and 2025 each had 32. This year already 39, and the sunny half of the year hasn't even started. 2026 is on a record pace.

Imbalance Between Generation and Consumption

Behind every negative hour is green energy that is produced but not demanded at that moment.

Without sufficient flexibility in the system, this imbalance grows with every additional gigawatt of renewable capacity.

System Integration as the Core Challenge

At the beginning of the renewable expansion, the power system could easily absorb fluctuating generation.

With further additions, the focus shifts: The integration of renewable energy (temporally, spatially, and economically) becomes the central challenge.

➡️ Negative power prices are not a problem of the energy transition, but a sign of its progress.

Globally, over 90% of new capacity additions already come from renewable sources. Surpluses are therefore not a flaw in the system, but a signal for more flexibility.

Battery storage, flexible loads, digitalization, and grid expansion will determine whether surplus becomes value creation — or waste.