The 2025 regional scenarios from distribution system operators (DSOs) serve for many developers and investors as an important reference framework for large-scale battery storage, battery storage projects, and expected BESS expansion. We compared these regional scenarios with the MaStR inventory (02/2026).

Three patterns emerged that are particularly relevant for project development, site strategy, investment, and the assessment of BESS forecasts.

Data Basis: 2025 DSO Regional Scenarios vs. MaStR Inventory (02/2026)

Comparing DSO regional scenarios with the MaStR inventory (02/2026) reveals how ambitious the modeled expansion paths for large-scale battery storage and BESS (> 1 MW) actually are and where regional focus areas and discrepancies are forming.

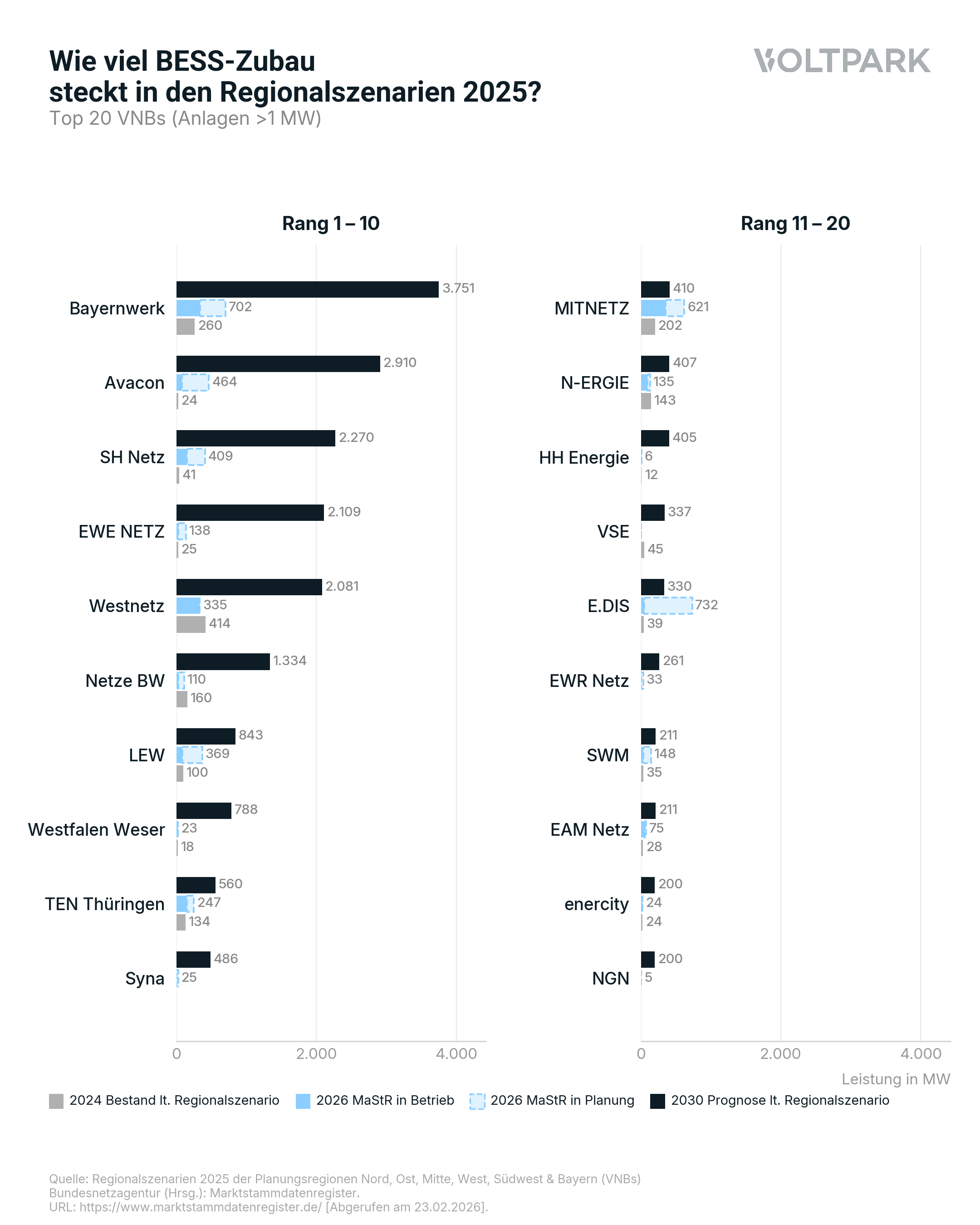

Pattern 1: High BESS Expansion by 2030 and Strong Regional Concentration

The cumulative BESS forecast from distribution system operators through 2030 stands at approximately 23.8 GW (> 1 MW). This is significantly above the level of other forecasts for all of Germany.

Notably, the regional concentration is striking: Over 70% falls on three planning regions.

- Central (approx. 6.5 GW)

- Bavaria (approx. 6.1 GW)

- West (approx. 4.2 GW)

This means: Large-scale battery storage is being heavily expanded, but not evenly distributed across Germany — rather regionally clustered. Clear clusters are visible at Bayernwerk, Avacon, SH Netz, EWE, and Westnetz.

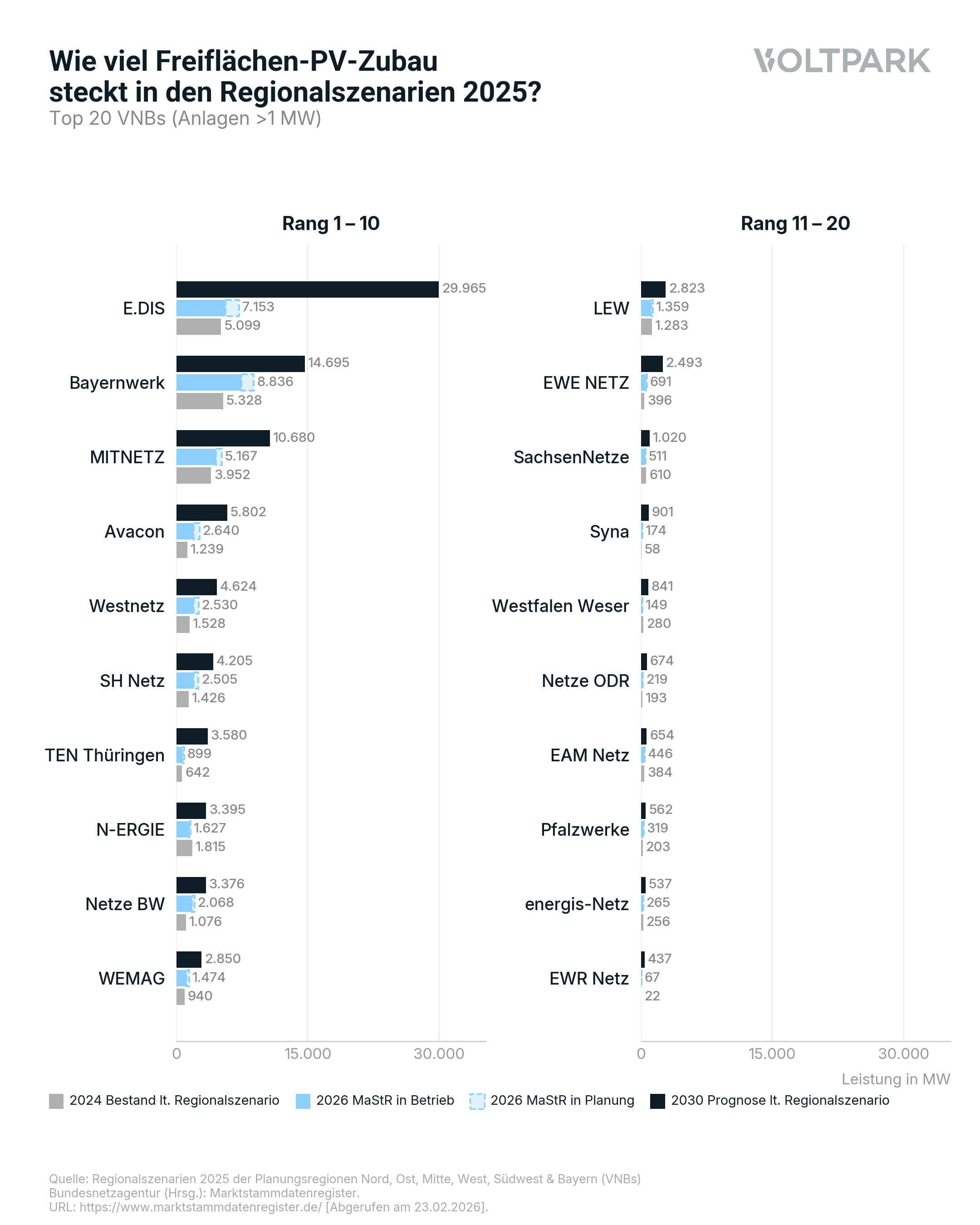

Pattern 2: PV and Storage Paths Are Diverging

In several PV-strong regions, the discrepancy between ground-mounted PV expansion and BESS forecasts is significant.

Example E.DIS:

- Approx. 30 GW ground-mounted PV expansion by 2030

- But only approx. 0.3 GW BESS forecast

We regularly hear from investors: Ground-mounted PV is hardly investable without storage. At the same time, DSO forecasts and market reality are diverging here.

Pattern 3: Significant BESS Expansion Also After August 2029

Several grid areas model significant BESS expansion only for 2030 to 2035. This contrasts with current market logic, which is heavily focused on COD ≤ August 2029 due to the AgNes grid fee reform.

Planned for 2030 to 2035 (from +21 GW to 45 GW):

- E.DIS approx. 3.2 GW additional BESS expansion

- Bayernwerk approx. 3.0 GW

- Westnetz approx. 2.2 GW

Assessment: What Does This Mean for Developers and Investors?

The patterns show: Storage is structurally anchored in grid planning. Regardless of regulatory uncertainties, a viable business model will emerge in the medium term. Because a power system with continuously increasing renewable shares is not viable — neither from a grid nor a market perspective — without flexibility and thus without storage.

Conclusion

The 2025 DSO regional scenarios point to very high BESS expansion by 2030, albeit with clear regional concentration. At the same time, PV-strong regions show partly significant deviations between ground-mounted PV expansion paths and BESS forecasts. And: Significant BESS expansion is modeled in several grid areas also for 2030 to 2035, despite current market logic around COD ≤ August 2029.