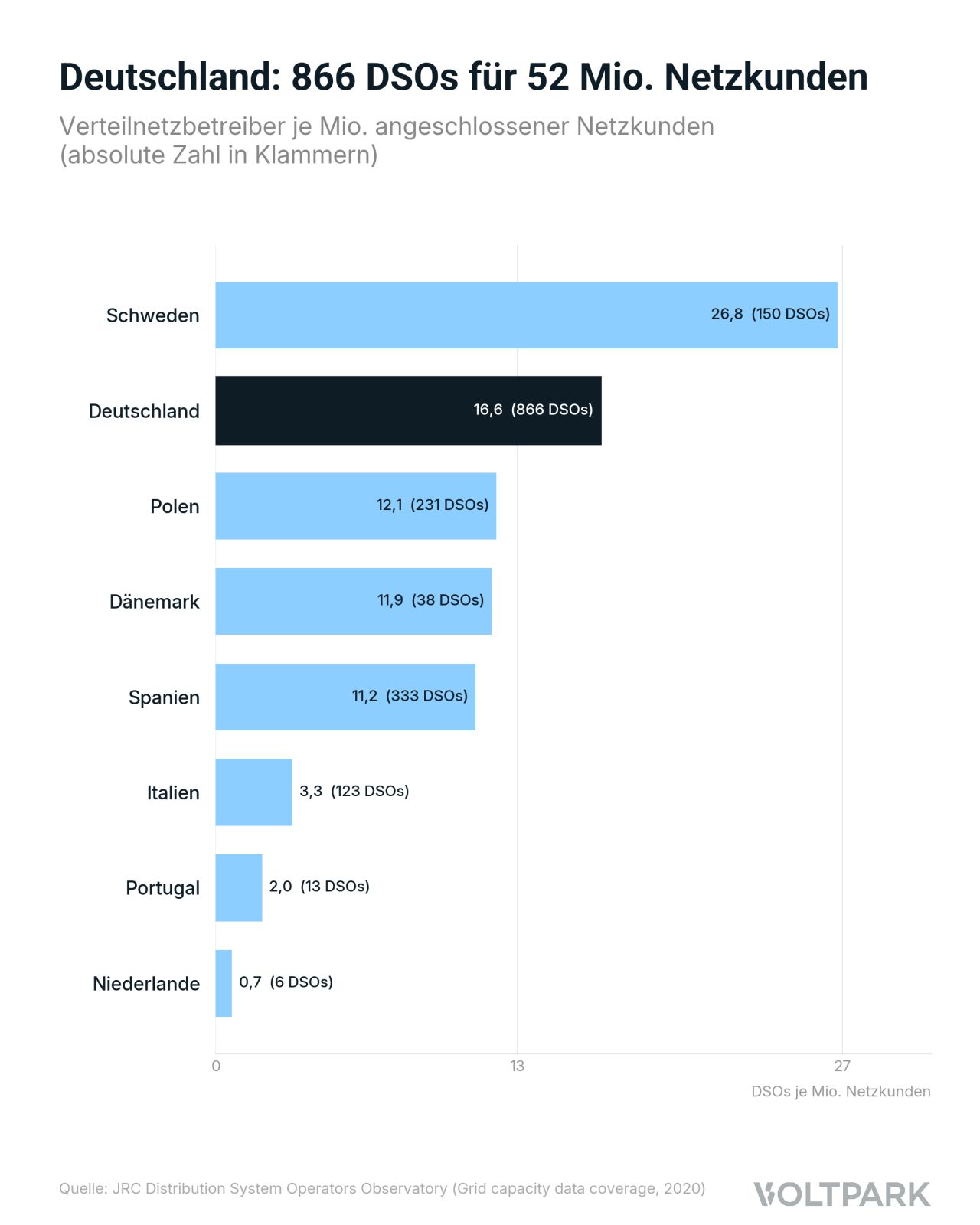

Anyone developing a renewable energy project in Germany doesn't negotiate with one grid operator – but with one out of 866.

866 distribution system operators (DSOs) serve 52 million grid customers in Germany. For comparison: Italy has 123 DSOs for 37 million customers, Spain 333 for 29 million, the Netherlands just 6 for 9 million.

For project developers, this means three things:

First: Every Grid Connection Is Its Own Project

Different connection conditions, different deadlines, different contacts. A process that in Spain covers 80 % of the market with three DSOs is hardly repeatable in Germany.

Second: Flexible Connection Agreements Vary Widely

For standalone storage and co-location projects, flexible connection agreements differ significantly between grid operators. Since this is so far a discretionary provision, DSOs handle the instrument with very different levels of professionalism – from simple static offtake restrictions to dynamic arrangements that are often more attractive for developers but place higher demands on grid operation and IT at the operator's end. This doesn't always make development easier, but it can be an advantage if you have already had positive experiences with a grid operator.

Third: Fragmentation Shapes the Transaction Market

DSO fragmentation also affects the transaction market. Identical projects can be valued differently depending on the grid area, because connection quality, curtailment history, and the maturity of the grid operator vary. In conversations with institutional investors, we observe that certain DSO regions are clearly preferred. This makes the grid area a factor that should be considered as early as site selection.

The Grid Area Is No Side Issue

Germany is Europe's largest renewables market, with the most liquid power markets. The 866 distribution system operators are no side issue here – they co-determine connection conditions, project economics, and transaction value. Anyone developing or buying here cannot do without local know-how and a systematic understanding of the DSO landscape.