Solar PV showed the way: for years, major institutions systematically underestimated the buildout, year after year. Each new forecast came in higher than the last. With battery storage, it is happening again.

The 2030 Forecasts Are Revised Upward Every Year

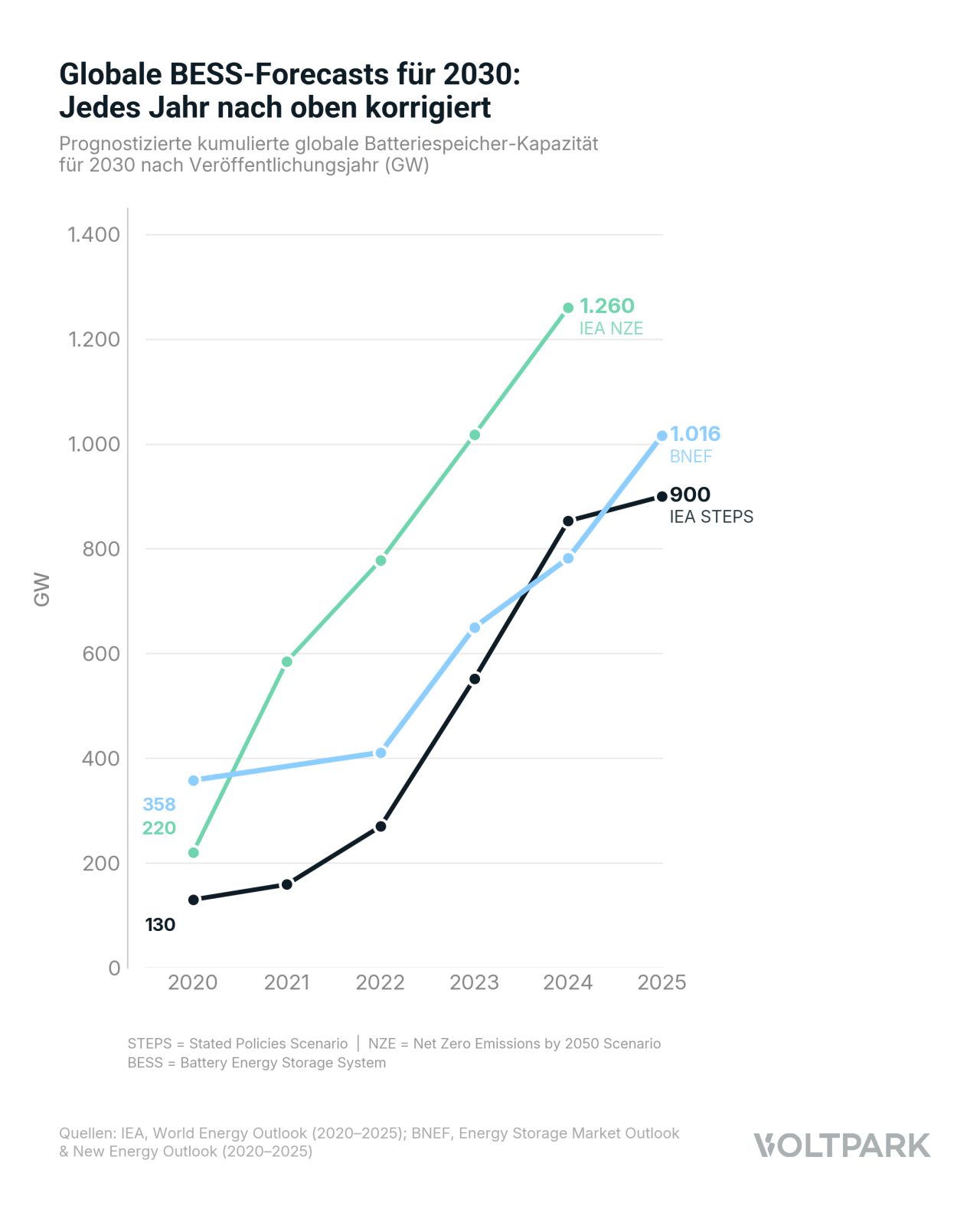

This is clearly visible in the 2030 forecasts for installed capacity made between 2020 and 2025:

➡️ IEA STEPS (Stated Policies Scenario): from 130 GW to 900 GW (roughly 7x).

➡️ IEA NZE (Net Zero Scenario): from 220 GW to 1,260 GW (roughly 6x).

➡️ BNEF: from 358 GW to 1,016 GW (roughly 3x).

The Reality Check

In 2025, around 110 GW of BESS was installed worldwide – of which 3.7 GW in Germany. That roughly matches the IEA's 2020 forecast (STEPS) for installed capacity in 2030 (130 GW). In other words: what counted as a target for the end of the decade back in 2020 is already annual buildout today.

Why Linear Models Fail

The reason is structural: linear forecast models break down in exponential markets. When battery costs fall sharply within a few years, when the industrial policy of many countries accelerates the buildout, and when China alone supplies around 60 % of global additions, traditional forecasting methods are systematically overwhelmed.

➡️ One can only hope that Germany stays on course in the BESS ramp-up – for example through clear and practicable rules on the privileged planning status of BESS under building law, as well as a consistently coordinated interplay of grid connection charges (BKZ), FCAs, and grid fees (AgNes).