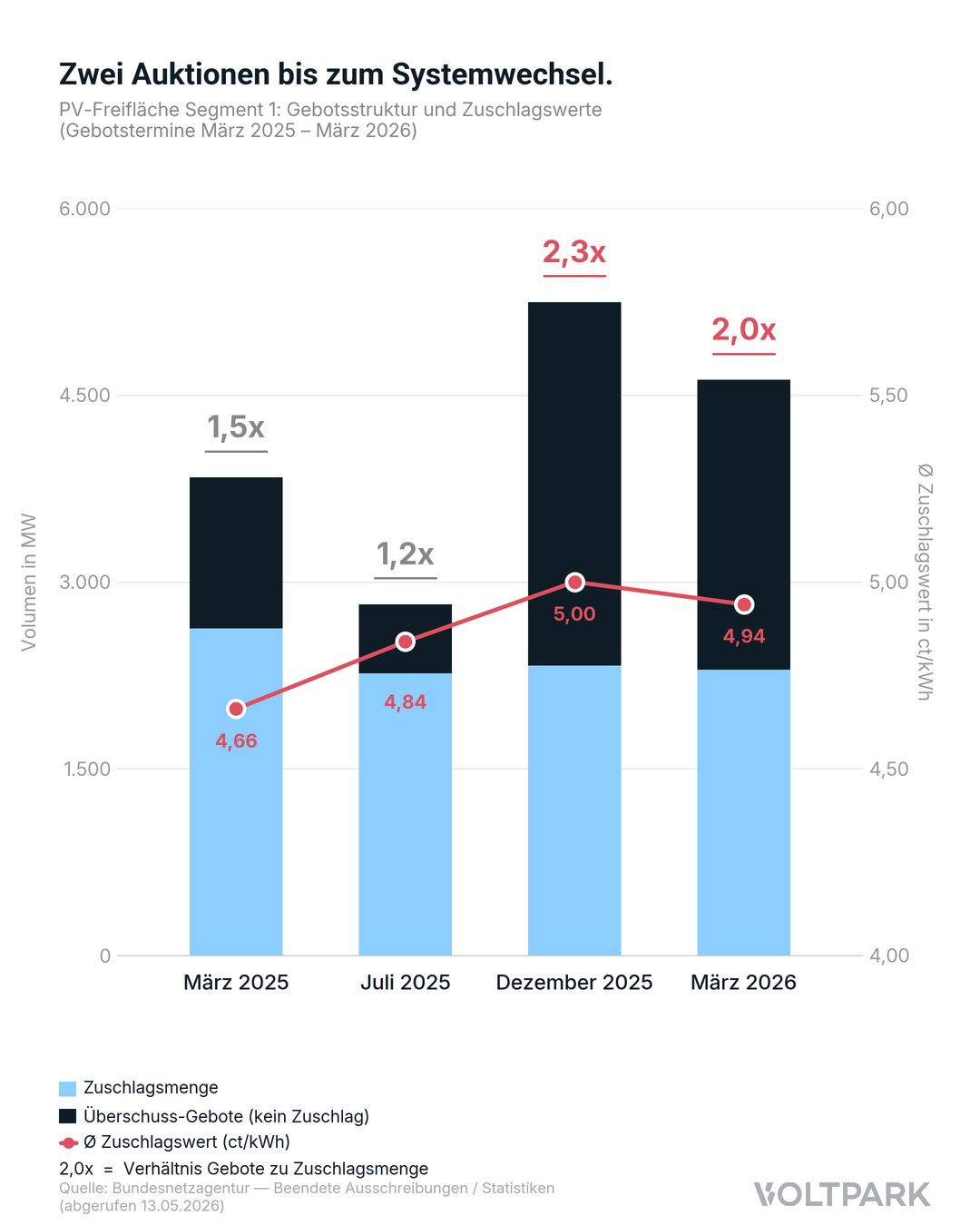

The March 2026 round for ground-mounted PV was once again clearly oversubscribed: 4,622 MW of bids faced 2,295 MW of tendered volume – a ratio of around 2.0. The volume-weighted award value was 4.94 ct/kWh, with successful bids ranging from 3.99 to 5.10 ct/kWh.

Tougher Competition – and Yet Higher Prices

The comparison is telling: twelve months ago, award values stood at 4.66 ct/kWh, with an oversubscription of 1.5. Today competition is significantly tougher, yet prices are around 6 % higher.

Two opposing forces are at work here. Competitive pressure is rising: more bidders, scarce award volume, a pull-forward effect ahead of the regime change. At the same time, however, the economic floor below which no reasonable bidder can go is rising. Three factors push it upward:

Cannibalization: The solar market value in April 2026 was just 1.317 ct/kWh – the lowest level since April 2020.

Negative price hours: These accumulate above all during summer midday hours – precisely when PV produces. Hours without remuneration noticeably reduce the effectively remunerated full-load hours. Anyone wanting to maintain the same IRR needs a higher award value.

Financing and CAPEX: After module prices fell for years, we are now seeing at least a stabilization, possibly a short-term trend reversal. In addition, trade conflicts and the Iran war are driving inflation and thus increasing the risk of interest rate hikes.

Two More Auctions Under the Familiar Regime

At least two auctions remain under the familiar regime until the system change: July 1 and December 1, 2026. At the end of 2026, the EU state-aid approval of the EEG 2023 expires. From July 2027, a clawback mechanism will apply to new installations above 100 kW, presumably as a two-sided contract for difference. Many details are not yet clear: strike mechanism, negative hours, assessment period, storage co-location.

➡️ For build-ready projects, this means two things. There are two realistic award opportunities under the familiar regime. Anyone left without an award in 2027 is planning against a mechanism whose valuation parameters only become calculable over the course of the year.