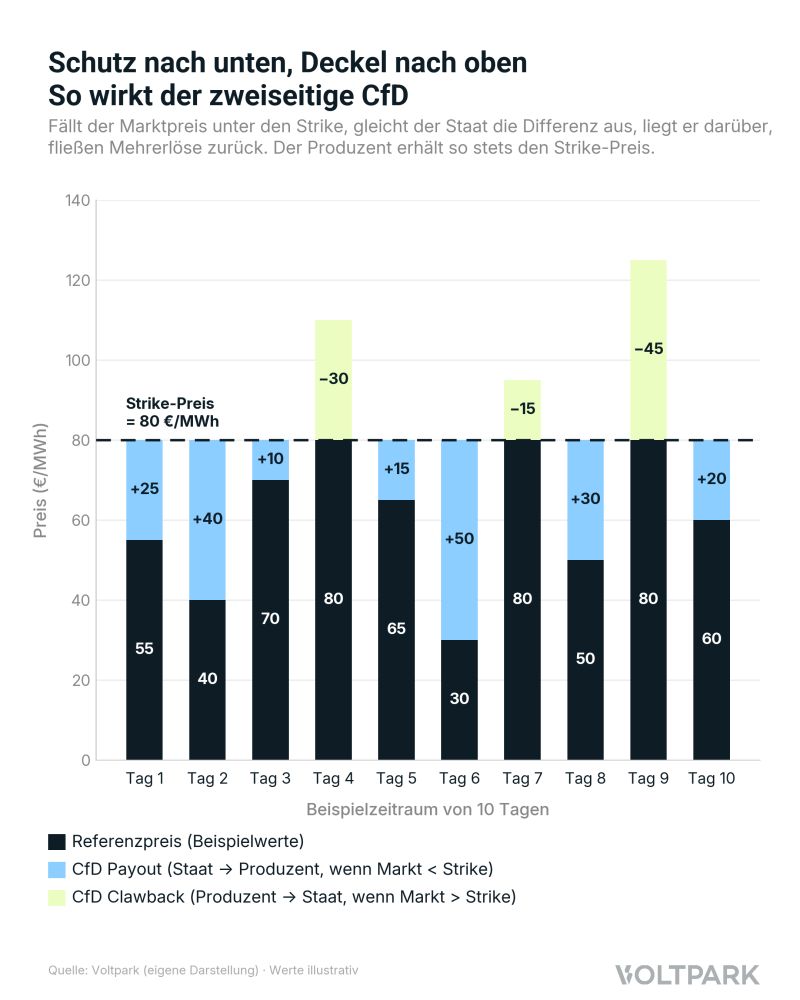

The working draft of the EEG 2027 makes ground-mounted PV the central expansion path: rising from 9.9 GW to 14 GW per year from 2027 to 2032. At the same time, the support scheme is being fundamentally rebuilt. The one-sided market premium gives way to a two-sided contract for difference (CfD) with a so-called “refinancing contribution.”

What's New?

Until now: if the market price exceeds the applicable value, the operator keeps the surplus. In future: if the technology-specific annual market value exceeds the applicable value, operators above 100 kW must pay back the difference as a refinancing contribution.

There is only a minimum revenue of 0.5 ct/kWh for solar, below which no clawback is allowed. The option to use high-price years as a buffer is thereby capped.

What This Means for Developers Today

1. Plan storage from day one. From mid-2026, the MiSpeL rule allows mixed operation for the first time: PV power (green, EEG-supported) and grid power (grey, market-price-based) in the same storage system. Anyone co-developing a green-power storage system today can capture the upside from grid charging once grid capacity later frees up – provided it is designed accordingly.

2. The 2026-vs-2027 cut-off becomes a valuation driver. Projects awarded before the EEG 2027 takes effect remain under the old market-premium logic – with full upside from high-price years and no clawback. Projects under the new regime, by contrast, will require structurally different bidding strategies: because bidders can no longer price in high-price years, award values are likely to rise on aggregate.

3. Diversify revenues. Which prices can be achieved under the new auctions is still unclear. Alongside classic PPAs, hybrid PPAs with storage or on-site PPAs can be sensible alternatives.

Nothing has been decided yet. But anyone developing projects today that will go online in 2027+ should prepare for the new reality.