There is hardly a topic that comes up more often at energy conferences in 2025/26 than “co-location.” Every developer is examining it, every investor is asking about it, every grid operator has an opinion. Yet when you look for projects actually realized in wind energy, the result is sobering.

We Analyzed the Market Master Data Register

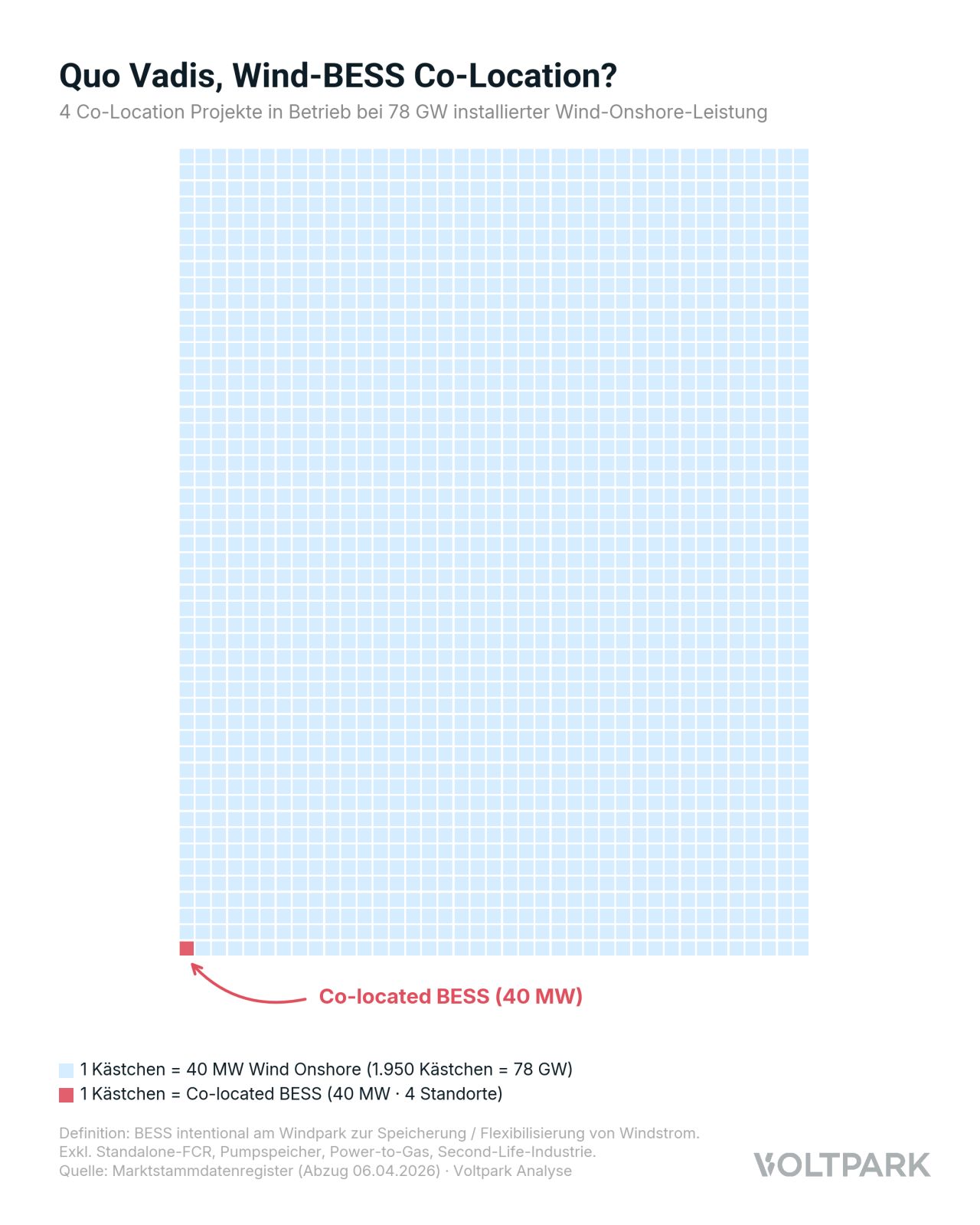

At Voltpark, we analyzed Germany's market master data register (Marktstammdatenregister) – via location ID, GPS matching, operator matching, and press releases – and verified each project individually. The basis is a strict definition: a BESS built specifically at the wind farm to store or flexibilize wind power – excluding standalone FCR, pumped storage, power-to-gas, and second-life industry.

Across 78 GW of wind and roughly 29,000 wind turbines, this definition yields exactly four operational wind-BESS co-location projects – totaling roughly 40 MW / 67 MWh.

The Four Realized Projects

1. BWP Reußenköge (SH) – Dirkshof: 302.6 MW wind, 32.8 MW / 56 MWh BESS.

2. Braderup (SH) – Bosch / Bürgerwindpark Braderup-Tinningstedt: 19.8 MW wind, 2.3 MW / 3 MWh BESS.

3. CEE Schmölln (BB) – CYCAP: 7.2 MW wind, 2.9 MW / 3 MWh BESS.

4. EnBW Häusern (BW) – EnBW Energie Baden-Württemberg AG: 6.9 MW wind, 2.2 MW / 4.5 MWh BESS.

The Structural Drivers Are Clear

➡️ The EEG award value for onshore wind is at its lowest level in eight years (5.54 ct/kWh, February 2026).

➡️ Co-location is prioritized by the legislator to make better use of scarce grid connections.

➡️ Battery storage CAPEX is lower than ever.

Even so: 40 MW against 78 GW of installed wind capacity. The narrative is far ahead of the market.

If we have overlooked a project, we welcome every pointer.