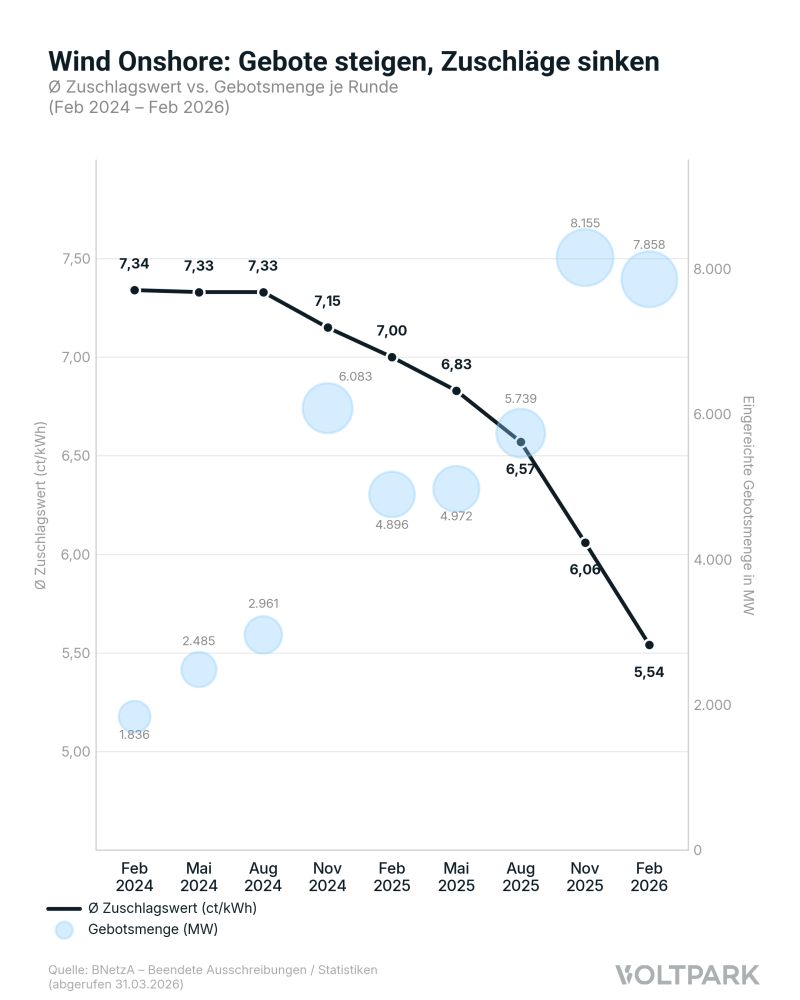

5.54 ct/kWh – the lowest volume-weighted onshore wind award value in eight years. This week, Germany's Federal Network Agency (BNetzA) published the results of the onshore wind auction for the February 1, 2026 bidding deadline. The figures paint the picture of a market under growing competitive pressure.

The Results in Detail

Against a tendered volume of 3,445 MW, bids totaling 7,858 MW were submitted – the seventh consecutive oversubscription. In total, the BNetzA issued 439 awards with values between 5.19 and 5.64 ct/kWh.

Two years ago, the average award value still stood at 7.34 ct/kWh. That marks a decline of roughly 25 % – while bid volumes rose significantly. The permitting pipelines are full.

Competition Is Working. The Margin Is Getting Tight.

539 negative price hours in 2025 and falling award values for onshore wind show that the revenue structure is already changing today. Anyone awarded at around 5.5 ct/kWh has correspondingly little buffer in their calculation.

Falling award values do not automatically mean falling levelized costs of electricity, but rather above all higher competitive pressure and a lower tolerance for error. Site quality, grid connection costs, and additional revenue streams are gaining importance in project development.

PV + Storage Is Already Standard. Wind + Storage Is Now Gaining Momentum.

Co-located storage shifts feed-in into higher-revenue hours, diversifies revenue sources, and uses existing grid connections more efficiently. Accordingly, many project developers are now concretely evaluating and planning the topic.

➡️ At award values like these, storage is no longer an optional add-on but is increasingly becoming a prerequisite for a viable project.